In the rapidly evolving FinTech landscape, data is power, and access to this data must be seamless but at the same time secure. FinTech companies offer novel services to sizable consumers; however, they must secure sensitive financial information against breaches, fraud, and any regulatory violations. The data security requires managing access privileges for internal employees, external partners, and global customers.

Identity Governance and Administration (IGA) platforms are systems designed to enforce data access control through automation, making it easier to maintain an amenable posture and minimize the risk of data breaches. On the other hand, FinTech companies are subject to constant scrutiny from regulatory frameworks, including the General Data Protection Regulation (GDPR), the Payment Services Directive 2 (PSD2), the Payment Card Industry Data Security Standard (PCI DSS), and the Sarbanes-Oxley Act (SOX). |Therefore, IGA is no longer a matter of choice for FinTech, but it is a matter of necessity for their survival and business growth.

Why Identity Governance Is Necessary in FinTech

Optimal Identity governance ensures security and scalability for the FinTechs simultaneously, meeting the particular access challenge of tech organizations:

- Avoid Insider Threats

Inappropriate privilege is the primary cause of data exposure. IGA systems enforce least-privilege access, limiting users to just what they need.

- Meet Compliance Requirements

IGA facilitates automatic audit trails and certifications, making smooth compliance with requirements such as KYC, AML, and GDPR.

- Reduce the Risk of Fraud

IGA continuously monitors user access and performs automatic role revocation to prevent unauthorized access, thereby preventing financial and reputational damages.

- Speed up Onboarding and Offboarding

IGA quickly grants provisions to new hires and swiftly revokes the provision upon termination, ensuring that access is strictly tied to employment.

Key features of IGA are briefly described below:

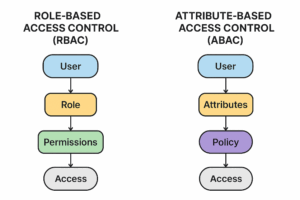

1. Role-Based Access Control (RBAC) and Attribute-Based Access Control (ABAC)

In a FinTech environment, data and resource access are granted based on intent, precision, and context. RBAC grants permission to users according to established roles. For example, a Loan Officer role in a financial organization should be allowed access to the loan origination systems. It is simple, scalable, and works well in structured environments. Similarly, ABAC makes decisions by utilizing dynamic attributes, such as location, time, or risk level. For example, Only traders in the EU can access GDPR-protected data during business hours. Furthermore, ABAC provides the utmost granularity, making it especially suitable for compliance-heavy workflows and remote-access scenarios. However, IGA platforms in FinTech enable you to combine both for maximum flexibility and control.

2. Access Certification & Recertification

Certain regulatory compliances demand continuous review of user access in FinTechs. The IGA systems automate any workflow related to user access certification so that only authorized users retain access to sensitive systems. The automation satisfies the audit requirements, thereby reducing the likelihood of human error.

Key Elements:

- Automated access reviews- Managers are prompted on schedule to review user rights

- Quarterly recertification audits- Such as those required by SOX and PCI DSS

Automation eliminates administrative effort and provides a stronger defense for compliance during audits.

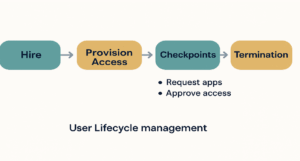

3. User Life Cycle Management

In a FinTech environment, user access throughout one’s employment journey must be closely monitored. IGA platforms have matured to automate the entire user lifecycle operationsfrom onboarding to offboarding, so that no delays and no unauthorized access are permitted.

- Auto-provisioning: |IGA grants instant access upon hiring to the required systems based on the employee’s job or department

- Auto-deprovisioning: IGA revokes all access rights to the employee, preventing any security breach

- Self-service access request: Employees request access to data and resources that allow built-in approval workflows, thereby freeing IT from delays

By following the protocol depicted in Figure 3, authorized access is provisioned while maintaining efficiency and adhering to policies.

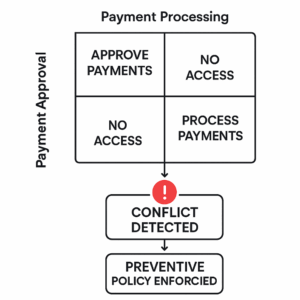

4. Segregation of Duties (SoD) & Policy Enforcement

Segregation of Duties (SoD) in a FinTech ensures that bopunderies are set to prevent conflicts in access rights by a single individual that may lead to fraudulent activity. In a FinTech, example roles of SoD include:

- When User A sends a funds transfer, they should not be able to approve the same transaction

- The compliance officer should not have the authority to edit transaction data

Furthermore, IGA platforms double down on SoD by:

- Setting risk-based access policies

- Flagging/blocking SoD violations based on these policies automatically

Implementing the scheme illustrated in Figure 4 strengthens internal control and serves as a safeguard against insider threats.

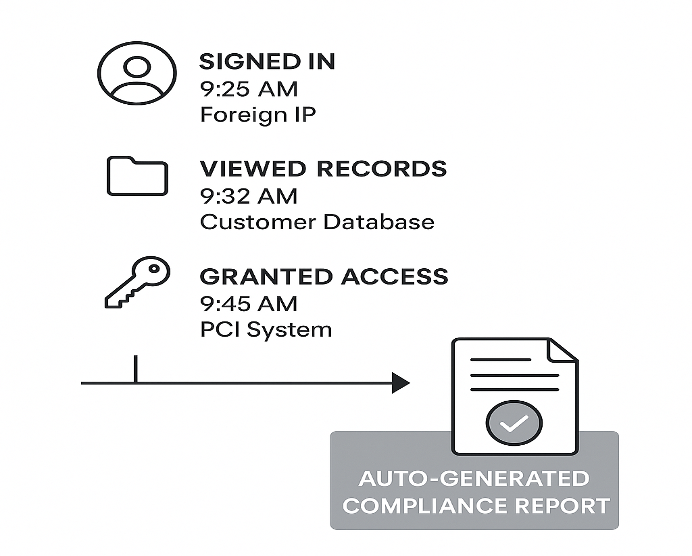

5. Audit Standpoint: Logging & Reporting

“Traceability’s a must,” FinTech says, “for every access action.” Therefore, IGA platforms generate access logs that reveal the who, what, when, and why behind access, providing an audit trail for self-audits or external inspections to ensure regulatory compliance.

- Logs are generated in real-time, allowing anyone to see what’s happening instantly

- Compliance reports are generated by FINRA, FFIEC, and other regulatory bodies for auditors

The logs shown in the figure below are used for forensics, assurance of accountability, and compliance.

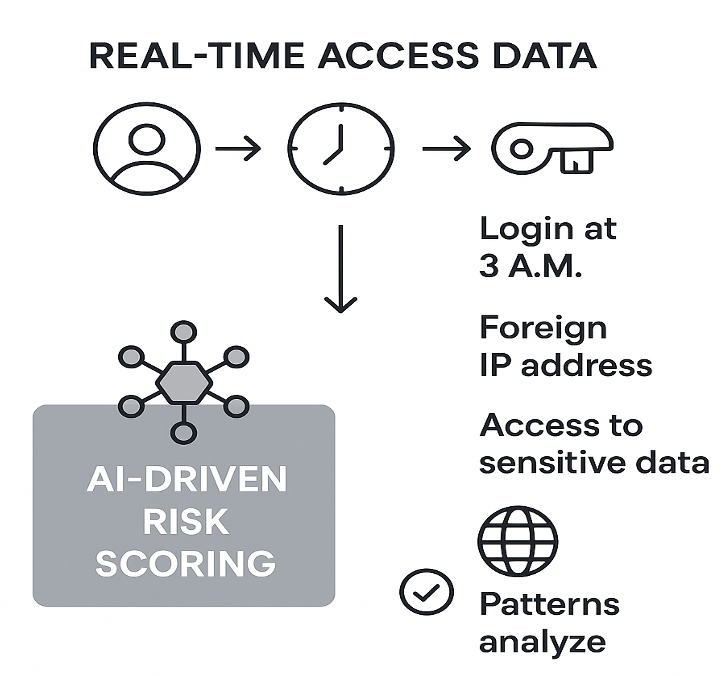

6. AI-Driven Anomaly Detection

State-of-the-art IGA systems offer AI algorithms to detect abnormal access that traditional rules-based systems may overlook. Such tools perform continuous analysis of the user behaviour and flag any abnormal behaviour, such as:

- Logging in at an odd time (like at 3 AM)

- Accessing sensitive information from an unknown IP or device

- Attempting unauthorized escalations of privileges

In IGA systems, a narrative risk score is assigned to each user, allowing the security team to prioritize investigations and respond accordingly. These measures help prevent insider risk, which can be difficult to recognize without behavioural context when there is either malicious intent or negligence.

The above figure illustrates that AI functions as intelligent, real-time governance for access control prevention in FinTech.

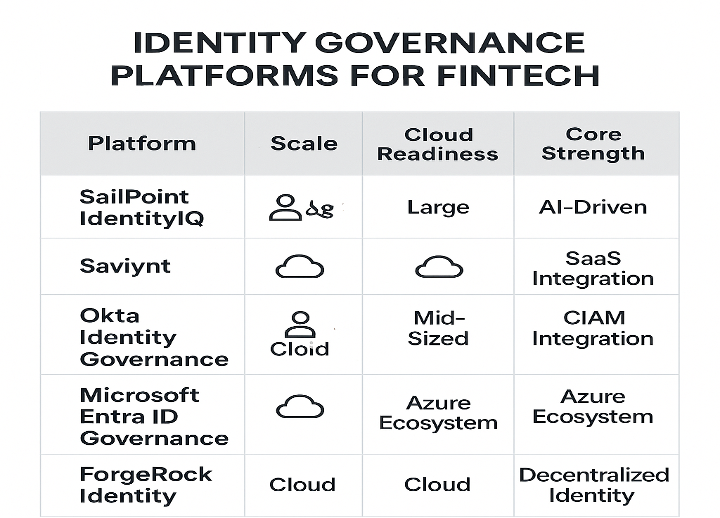

Leading Identity Governance Platforms for FinTech

The choice of an IGA platform depends significantly on the organization’s size, infrastructure, and compliance needs. Here is a brief comparison of some of the major IGA solutions:

- SailPoint IdentityIQ: Designed for large financial institutions, the solution provides heavy compliance capabilities and AI-based access insights in complex hybrid environments

- Saviynt: The solution is optimal for cloud-native FinTechs. For instance, Being’s SaaS integrates well with AWS, Azure, and Google Cloud

- Okta Identity Governance: The solution is well-suited for mid-sized organizations. A remarkable feature of the solution is its fast deployment and out-of-the-box CIAM integration

- Microsoft Entra ID Governance: The solution is recommended for companies deeply embedded within the Azure/Microsoft 365 ecosystem

- ForgeRock Identity Governance: The system supports open banking and DeFi platforms. Furthermore, it supports blockchain and decentralized identity protocols

IGA Implementation Checklist for FinTech

To implement a robust IGA framework, the FinTech organizations should carry out the following steps:

- Define Access Policies – Generate RBAC, ABAC, and SoD rules in accordance with business roles and responsibilities.

- Integrate with HR Systems – Automate employee onboarding and offboarding to ensure access is updated in real-time.

- Allow Self-Service Access Requests – Remove any potential bottleneck from IT while increasing user autonomy in access requests.

- Set Automated Certifications – Configure compliance to be reviewed quarterly.

- Use AI Anomaly Detection – Go on the offensive against riskier behavior.

- Generate Compliance Reports – Always be up to date on regulators’ audits.

It is a good practice to run these steps iteratively to accommodate changing risk and compliance needs.

Future Trends of Identity Governance in FinTech

Identity governance is evolving rapidly to meet the increasingly digital and decentralized financial ecosystems of FinTechs, with the following being key trends shaping the future:

- AI-Powered Access Governance – Effortless revocation of stale privileges and accurate prediction of access risks.

- Decentralized Identity (Self-Sovereign Identity) – Through the use of blockchain, end-users retain control over their credentials and simultaneously enhance their security.

- Passwordless Authentication Integration – Fusing IGA with FIDO2, biometrics, and MFA to diminish password dependency and enhance access resilience.

These disruptors are rapidly revolutionizing identity management in a FinTech world that is cloud-first and mobile-driven.

Conclusion

For the maintenance of sensitive financial data, IGA platforms are a must for FinTechs. They serve to protect against insider threats, ensure compliance is automated, and scale securely as the business grows. Now is the time to adopt an IGA framework; your regulatory posture, customer trust, and operational integrity depend on it.

Anant is a lead Cybersecurity Engineer,CIAM certified, building IAM solutions for Organizational Cybersecurity with strong foundations in Enterprise Integrations and Technical Leadership. Started his career in Enterprise Middleware technology as middleware engineer, groomed by Enterprise architects early in the career helped laid strong foundation in Enterprise architecture design and patterns, early adopter of API programming built software productivity tools for companies leveraging native API methods provided by product framework. Recent experience in Cybersecurity with focus on Identity and Access Management in Information Security.

The opinions expressed in this post belong to the individual contributors and do not necessarily reflect the views of Information Security Buzz.